Housing Loan Rules & Regulations, Guidelines for Home Loan

Updated: Sep 13, 2022

Did you know? Homeownership is one of the most important dreams for most Indians. People wish to buy a house and build a family in it. More than a nest, home ownership these days is more like having a long term asset, especially for those who wish to leave behind legacies for their future generations.

To make home purchasing an achievable goal, the concept of housing loans came into the picture. At SMFG India Home Company, also known as Grihashakti, our goal is to help each and every Indian get access to affordable financing so that they can purchase their dream home.

What are Home Loans?

A Home loan is a form of secured loan that you can take up from various financial institutions, for the sole purpose of purchasing a home. This home could be a newly constructed property, a resale property, or an under construction property. In exchange for giving you a loan, the house is placed as mortgage or collateral with the lender. Once you repay the loan, the deeds to the home will be given back to you, and all consequent property records will reflect that you are now the rightful owner of said property which is no longer under mortgage. In case of default, the lender has the right to repossess the property, and sell it in order to reclaim any losses.

Housing Loan Rules and Regulations

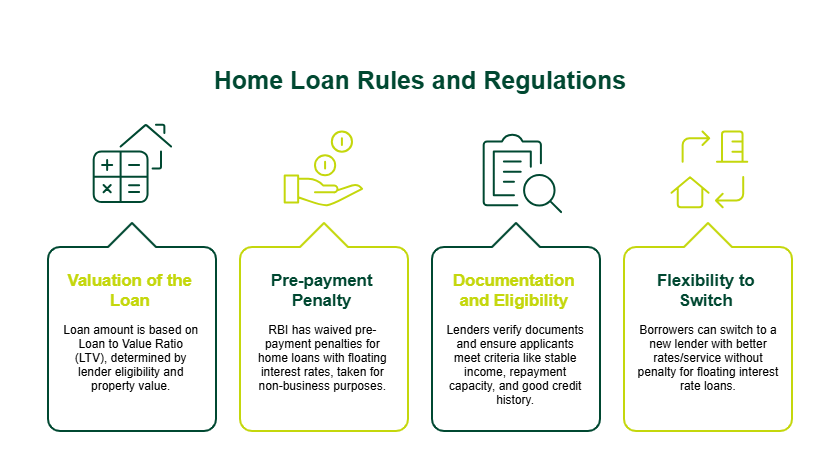

Like for every other loan, there are home loan rules and regulations. The process of getting a home loan in India is heavily regulated by the Reserve Bank of India (RBI) as well as the National Housing Board (NHB). Some of the key rules and regulations are:

Valuation of the Loan

The loan offered by financial institutions or banks is done based on the Loan to Value Ratio (LTV), which is in turn determined based on the lender’s eligibility as well as the nature & value of the property pledged. Under LTV, the bank will guarantee funds up to a certain limit (percentage) only. RBI has set the new home loan rules as:

- LTV stands at 90% for a loan of INR 30 lakhs and below.

- LTV stands at 80% for a loan that is above INR 30 lakhs but within INR 75 lakhs.

- LTV stands at 75% for a loan that is INR 75 lakhs and above.

The loan amount is calculated based on the property value and does not include stamp duty, registration charges, and other such expenses.

Apply Now

Pre-payment penalty

Home loans are usually high-value loans for which people choose a duration of 10 to 30 years for repayment. Earlier if one chose to pre-pay the liability amount and settle the loan, a penalty of 2 to 5% was levied. According to the new rules, RBI has made home loan rules and regulations in India is made more flexible and favorable for borrowers thereby, waiving the penalty/charges. This is applicable in the case of home loans with a floating interest rate component, taken for non-business purposes.

Documentation and Eligibility

The lender of the loan needs to ensure that all the documents provided by the public are in order with the statutory requirements. Also, home loan applications shall be accepted by people who meet the eligibility criteria; it means they must have a stable income, sufficient repayment capacity, a good credit history and a CIBIL score of 700 and above. This must be verifiable with the help of documents. Depending on the lender, other criteria may also be applicable.

Must Read: Tips to improve your CIBIL score immediately

Flexibility to switch

If you have taken up a home loan when the interest rates were high, and now you have found a lender who is willing to transfer the balance of your principal amount outstanding at better rates / service, you have the option to to foreclose a loan without penalty and switch to a new one with a lesser interest rate. One can use this advantage in the case of floating interest rate loans taken for non-business purposes only. Some lenders may also have clauses related to the source of financing for closing out the principal amount outstanding.

These are some of the housing loans and regulations. As these are statutory points, there are also some other guidelines for home loans that you may find useful.

Guidelines for Home Loans:

- Building up a good credit score is important. Thus, if you take up EMI’s or credit card dues, repay them on time. Ensure that your existing debts (including cards) are less than 30% of your monthly income to get the best deal for a home loan.

- Know your requirements. Choose the type of loan; fixed or floating interest rate loan as per your convenience.

- Make a big down payment to the extent possible. It helps you save on heavy principal and interest costs.

- Even though home loans allow you to borrow for a longer tenure, try to shorten it. It helps you save on high-interest repayment.

- Make part prepayments towards your home loan whenever you get any extra income such as a bonus from work, or a particularly good business season. Paying even as much as 1 extra EMI every year could work wonders in terms of helping you close your loan more quickly and save on the total interest outgo.

- Purchasing home loan insurance helps guarantee your family’s security in case of unforeseen situations.

Also, ensure you go through all the required documentation carefully.

Conclusion

In an ideal world, we all would have the money to fulfill all our dreams. But in reality, we are making some major dreams possible. Thus, don’t hesitate to fulfill your goal of purchasing a home today.

Must Read: What is Part Payment on Home loan

Disclaimer: *Please note that this article is for your knowledge only. Loans are disbursed at the sole discretion of SMFG Grihashakti. Final approval, loan terms, disbursal process, foreclosure charges and foreclosure process will be subject to SMFG Grihashakti’s policy at the time of loan application. If you wish to know more about our products and services, please contact us.